CIO Update: Once again, overweighting commodities

14 JUL, 2026

By Philipp E. Bärtschi, CIO at J. Safra Sarasin Sustainable AM

AI Drives Growth in the United States

Investment in AI-related infrastructure remains the main growth driver in the United States, supporting the manufacturing sector, labor demand, and corporate earnings. Meanwhile, private consumption continues to show notable resilience despite falling real disposable income, helped by wealth effects and a lower savings rate.

As inflationary pressures continue to build, the Federal Reserve has essentially abandoned its accommodative monetary policy. In his first meeting as the Fed's new chair, Kevin Warsh did not oppose the FOMC's shift toward a more restrictive stance, reaffirming the 2% inflation target and leaving the door open to further rate hikes.

While the widespread adoption of artificial intelligence could ultimately have a disinflationary effect in the long run, current indicators suggest its real-world application still lags behind its theoretical potential. As a result, AI is unlikely to have a significant impact on monetary policy in the near term.

The eurozone remains the weakest link among the major developed economies. Growth momentum stays subdued, the output gap remains negative, and the fiscal stimulus from Germany's economic recovery package has so far disappointed. Nonetheless, inflation remains too high, which led the European Central Bank (ECB) to raise interest rates in June. Even so, we expect only one further hike, as economic conditions are considerably less inflationary than in 2022.

The UK economy, meanwhile, continues to face a difficult mix of weak growth and persistent inflation. However, the cooling of economic activity is allowing a gradual easing of the labor market, which could make further monetary tightening unnecessary. With the upcoming leadership handover to Andy Burnham, markets remain watchful for further details on his policy agenda, which is likely to increase sterling volatility in the near term.

Japan's economy continues to benefit from broad fiscal support, positive real wage growth, and solid semiconductor demand. Yen weakness continues to support exports, while energy subsidies have limited the impact of higher oil prices on inflation. The Bank of Japan is likely to maintain its gradual policy normalization strategy, so we expect yen weakness to persist for now. We also do not rule out further currency market intervention, given that the trajectory of global yields remains unfavorable for the Japanese currency.

In China, growth momentum has moderated relative to the strong performance seen in the first quarter. AI-related exports and clean energy supply chains continue to show strength, but domestic demand, consumer confidence, and corporate earnings have weakened. The real estate correction has eased somewhat, though the adjustment process is still ongoing.

Elsewhere in Asia, economies integrated into AI-related supply chains remain in a relatively better position than energy-importing countries, which have been hit hardest by the oil shock linked to the conflict with Iran.

Headwinds from Dollar Strength

Equity markets have broadly moved sideways in recent weeks. While some indices, such as the Swiss Market Index (SMI), have reached new highs, other markets have posted slight declines. This divergence reflects, on one hand, the strengthening of the US dollar and, on the other, a market rotation toward more defensive sectors.

We expect emerging market equities to remain under pressure in the coming months. First, a stronger dollar tends to weigh on these markets, as it favors the repatriation of capital flows into dollar-denominated assets. Second, Chinese equities remain weighed down by weak domestic demand and deteriorating corporate earnings. Third, former emerging-market growth engines such as South Korea and Taiwan are being affected by the current sector rotation.

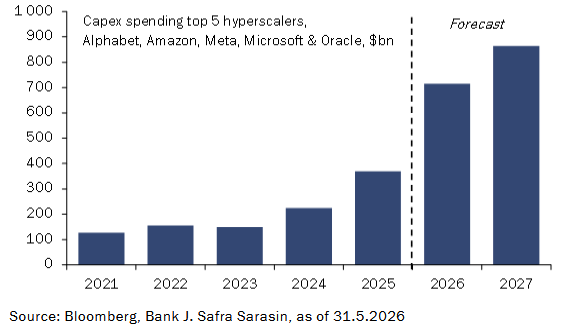

Although the structural AI theme remains fully intact, consolidation in the tech sector is likely to continue. It therefore remains essential to take a selective approach and focus on companies best positioned within the AI value chain.

We maintain a constructive view on equities heading into year-end, supported by solid corporate earnings, momentum in AI investment, and somewhat more attractive valuations in the United States.

Asset Allocation – Tactical Reallocations

Given that the macroeconomic outlook and corporate earnings growth remain favorable, we maintain a slight overweight in equities. However, toward the end of the second quarter we shifted part of our exposure from emerging market companies to developed market companies.

In doing so, we locked in part of the gains accumulated after the strong rally of recent months, while also taking into account the challenges that higher interest rates and a stronger dollar pose for emerging markets.

We maintain a slight underweight in fixed income. Within alternative investments, we have carried out a new tactical reallocation. The drop in energy prices has triggered a significant decline in commodity prices. Given the favorable economic outlook, we view this correction as an opportunity to move back into an overweight position.

By contrast, we have reduced our gold exposure to a neutral position. Higher interest rates and dollar strength are likely to limit the upside potential for precious metals in the near term.