Why Emerging Market Debt Should Not Be Generalised

9 JAN, 2025

Emerging market debt encompasses a variety of assets whose performance depends on factors such as credit quality, currencies and country-specific economic conditions. In 2024, while US dollar-denominated sovereign and corporate bonds showed positive returns, local currency bonds faced challenges caused by a strong dollar. This analysis highlights why generalising across this asset class can lead to the wrong conclusions and highlights the differentiated opportunities that emerging markets offer.

Author: Elisabeth Colleran, Portfolio Manager Emerging Markets Debt at Loomis Sayles.

The lack of uniformity across asset classes under the emerging market debt umbrella points to a myriad of factors that can influence performance. We believe that the sector's multi-faceted offerings, which vary by country, credit quality and currency, may mean more choice for investors - offerings that are best examined with a fine-tooth comb.

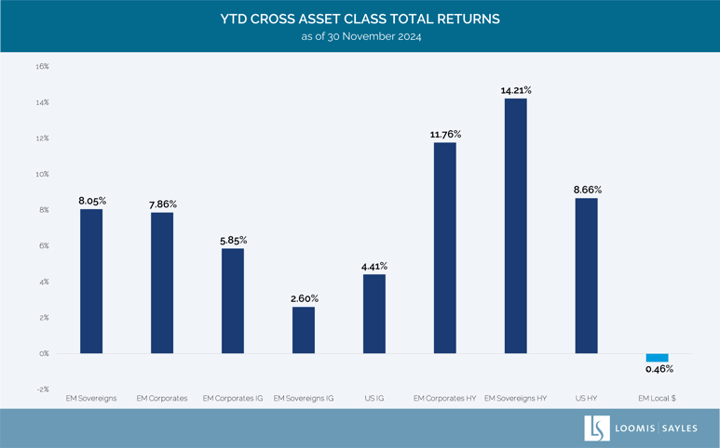

There is often no distinction between the characteristics of emerging market local currency bonds and those of emerging market corporate and sovereign bonds issued in US dollars. The chart below shows one reason why we believe that emerging market fixed income should not become generalised.

From January to November 2024, US dollar-denominated emerging market sovereign and corporate bonds have delivered positive returns, while emerging market local currency government bonds have struggled against a strong US dollar. In particular, US dollar-denominated emerging market corporate bonds have outperformed their US investment grade and high yield counterparts. Currency volatility is often in the news, but the problems affecting the local currency index have had little impact on the performance of the emerging market hard currency asset class, which has continued to benefit from domestic economic growth, strong corporate fundamentals and easing global interest rates.