Investing in European Commercial Real Estate

By: Philipp Wass, managing director, corporate ratings, Scope Ratings.

Issuers at the edge of investment grade as well as high yield continue to face a significant funding challenge.

Debt markets are slowly reopening for European commercial real estate companies, but investor confidence has not yet returned to pre-2022 levels due to high leverage, heavy capital investment and governance concerns for some issuers.

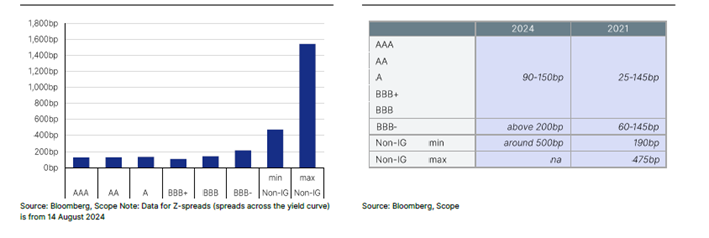

Only companies with a strong BBB credit rating or higher have access to the most liquid debt capital markets. Falling bond yields and tightening spreads can provide capital markets-based financing that is competitive with secured bank loans. For these issuers, spreads on new issues range from 90bp to 150bp, close to the 25bp-145bp range in 2021 (Charts 1, 2), the year in which capital market debt issuance for real estate companies peaked (Chart 3).

For companies at the borderline of investment grade - rated BBB - investors' fear of a downgrade translates into much wider spreads. Spreads on new issues are in excess of 200 basis points, which contrasts sharply with the 60-145 basis point range in 2021.

While we believe prices have bottomed in some property classes, investor nervousness also points to the risk of further falls in property values at the riskier end of the European commercial real estate market. Banks' appetite for financing less attractive commercial real estate remains low, exposing property managers to a negative loop. Sales of distressed assets may challenge current valuations and become a catalyst for balance sheet restructuring. In addition, potential sales of open real estate funds to offset cash outflows will test the resilience of the market.

Chart 1: European commercial real estate sector aversion: Z-spreads by issuer rating

Chart 2: Yield spreads of new European commercial real estate corporate bond issues

Non-investment grade issuers continue to face tough funding challenges.

Spreads are even wider for below investment grade issuers and companies where investors are concerned about governance. In practice, debt capital markets do not offer them a source of funding to avoid potential covenant defaults and support interest coverage ratios.

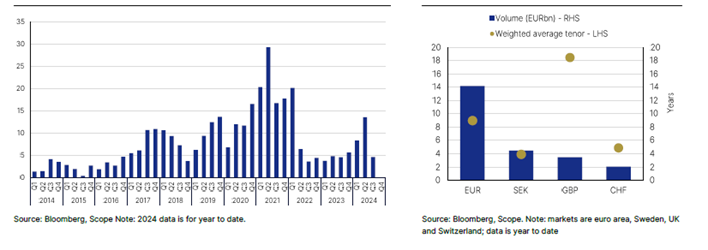

Europe's smaller capital markets, such as Sweden's, only offer borrowers credit at shorter maturities (chart 4) and thus provide little relief to a debt-laden industry.

Chart 3: Bond issuance of European real estate companies 2014 - 2024 (€m)

Chart 4: Bond issuance by selected markets (M €)

The risk of further declines in real estate valuations hangs over the sector.

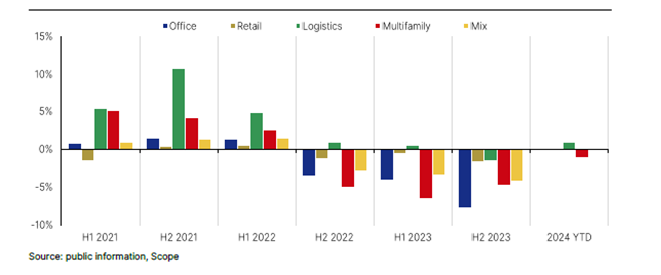

Investor caution also reflects the considerable risk that remains of further devaluation of real estate assets. Corrections in prime real estate assets (retail and office), as well as in residential and logistics real estate in general, are bottoming out (chart 5). However, prices of non-prime assets and those requiring heavy investment - modernisation, environmental compliance, conversion to adapt to structural changes in real estate demand - continue to fall.

Open-ended real estate funds, which are experiencing large cash outflows, could put additional downward pressure on valuations if they start to shed less attractive properties from their portfolios to raise liquidity. So far, funds have avoided doing so in order to keep their net asset values high. For example, if a substantial part of real estate - such as part of the EUR 128 billion in investments held by German open-ended funds - were to come to market, we would see further devaluations of real estate assets.

Chart 5: Average annual valuation of the value of a sample of 53 real estate companies (% change in the first half year)

A sharper turn in the interest rate cycle offers the possibility of further relief

European real estate companies would clearly benefit, like any indebted sector, from a sharper than expected turn in the interest rate cycle if fears of recession and stagnant growth translate into looser monetary policy in Europe and the US. At present, we expect continued cautious interest rate cuts, with a single 0.25 basis point cut by the ECB and the Federal Reserve during the second half of the year.

Underlying average interest rates have fallen sharply on fears of a US recession. Should weaker growth prospects materialise, as well as sluggish economic growth in the UK and the EU, faster interest rate cuts could provide a fundraising opportunity for companies with structurally sound asset portfolios, low leverage and no governance issues.

In general, we expect few short-term issues by smaller real estate companies (gross asset value of less than 2 billion euros) in the Eurobond market. The benchmark bonds that these companies issued to take advantage of low market funding costs in the decade leading up to 2022 have left many with the headache of refinancing them at much higher rates today, if at all.

Banks continue to support the sector... to a certain extent.

Banks have become more cautious and selective, but they continue to lend to the sector. They are willing to roll over existing financing for operationally sound property or real estate portfolios, and are even willing to extend new loans if collateral is strong and commitments are strict.

Spreads on secured loans have increased to 60-230 basis points depending on the type of property, the ultimate tenure, the leverage and, most importantly, the location. Bank financing may therefore be a more reasonable alternative for weaker creditors than capital market-based financing.

However, bank financing has its limits. Banks have not only tightened lending guarantees, but have become more focused on the composition of their loan portfolios with respect to maximum exposure to a sector, individual issuers and/or properties without good energy efficiency certifications or other green building ratings. Secondly, highly leveraged transactions are no longer viable, which means that if a borrower has financing problems, it may have to turn to the grey debt markets at a much higher cost.

Secured bank loans can only cover a marginal part of the refinancing of maturing bonds, leaving lower investment grade and non-investment grade issuers under pressure to restructure their assets or liabilities - or both - to protect their solvency, most likely at a high cost to both shareholders and debt holders.

European real estate companies as a whole have weathered the worst of the recent funding crisis, but the credit outlook for many companies remains highly uncertain.