US High Yield: Forget about spreads, focus on yields

17 FEB, 2025

By Bryan Petermann

Author: Bryan Petermann, Portfolio Manager at Muzinich & Co.

2024 provided credit investors with another year of very strong returns; high yield and leveraged loans delivered high-single digit gains, while investment grade fought off the impact of a steeper yield curve to deliver positive results.

Spread tightening in high yield offset higher rates and saw the broader market deliver slightly above carry-level returns. Steady earnings growth (aided by moderating inflation), favourable credit rating migration and low default rates enabled spreads to reach 10-year lows before settling back above 300 basis points (bps) by year end.

Moving into 2025, with tight spreads, a new US administration and increasing uncertainty over the interest rate trajectory and inflation, can US high yield continue to offer compelling returns? And what should investors look for when assessing the asset class?

Getting technical

In our view, technicals (supply and demand factors) should remain supportive. We believe the trend of persistent inflows into the asset class that began late 2023 should continue, with investors attracted by elevated yields and exposure to parts of the market that could benefit from policies focused on deregulation and domestic growth.

At the same time, we expect net new issuance to rise; while this will create opportunities, it may also create volatility if funds need to raise cash to participate, or secondary market spreads are pushed wider by more attractive new issues.

Strong fundamentals

Fundamentals have scarcely been stronger, with the overall credit quality of the market continuing to improve. The universe is highly rated, with the majority of issuers (53%) rated BB – a 15% increase on where the market was in 2010. Upgrades are outpacing downgrades, and there are more rising stars (high-yield rated issuers being upgraded to investment grade) than fallen angels (investment-grade issuers being downgraded to high yield). Meanwhile, the proportion of secured bonds has doubled over the past 10 years, to 30%.

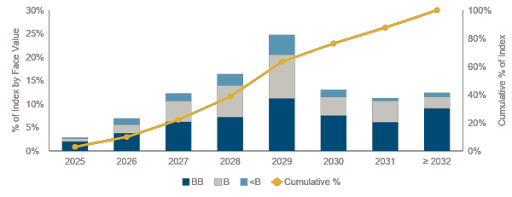

The default rate is at a historically low level – just 0.3% on a last twelve-month (LTM) basis. We believe this is likely to remain the case given the lack of upcoming maturities. The broader market also has a shorter duration than at any time since the Global Financial Crisis; maturities through 2026 are highly skewed towards higher-quality BB issuers and we believe markets will continue to be open to refinancings (Figure 1). Furthermore, we expect robust earnings and credit metrics to be stable over the short term.

Figure 1: Near-term maturities are being addressed

Rising uncertainty?

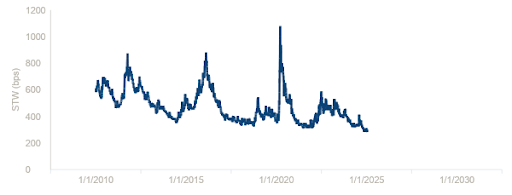

With such a supportive fundamental and technical backdrop, it is perhaps unsurprising markets are priced to perfection with spreads at 10-year lows (Figure 2) versus average non-recessionary spreads, which are around 500bps.

Figure 2: Spreads at 10-year lows

However, investors should be cognizant of the risks and possibility of higher volatility over the coming months. Inflation is slowly moving higher and new policies around tariffs and immigration could potentially limit efforts to tackle inflation and boost economic progress.

Some companies may have already exhausted their ability to pass through higher costs to their customers without a material impact on demand. ‘Animal spirits’ could lead to more aggressive use of debt for the benefit of shareholders, including share buybacks, M&A and dividends. As such, we intend to retain the flexibility to act opportunistically, taking advantage of any market and/or credit pullbacks.

Carry on

In terms of portfolio positioning, we will look to maintain a barbel approach focusing on carry and convexity. We believe this will allow us to take advantage of elevated yields and opportunities where bonds could pull-to-par relatively quickly due to M&A and/or refinancing transactions.

Given low dispersion in the BB/B segment, we favour moving up in credit quality. We will also look to limit exposure to issuers or sectors that could see their revenues or costs materially impacted by policy uncertainty (particularly related to trade and labour policy) and favour more domestically focused issuers and industries that could benefit from potential deregulation benefits.

To that end, we are constructive on telecoms/media, natural gas/midstream, utilities and financials, while remaining cautious on oil exploration and production, autos, chemicals, housing, gaming/leisure and discretionary retail.

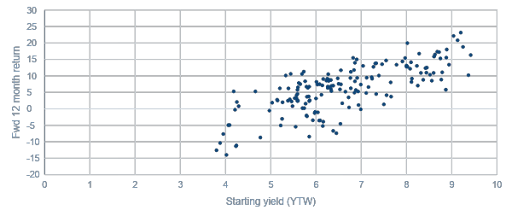

Figure 3: Yields vs returns, 2010-2024

In terms of potential returns, we see scope for net spread widening of around 50bps in 2025. In such an environment where spreads remain relatively tight, we believe carry is likely to be the main driver of returns.

Nevertheless, based on current yields, in our opinion it would approximately take a 200bps net move in rates/spreads for negative 12-month returns (over 300bps for short duration high yield). Based on our analysis, over the last 15 years and any time the market started with a yield over 7%, returns were positive for the next 12 months (Figure 3). We take comfort from this and highlight that the power of carry is a stronger factor than tight spreads when assessing the US high yield market.

Key Takeaways

- Fundamentals and technicals are likely to remain strong, despite uncertainty surrounding the new US administration, inflation and rates.

- We will seek to increase credit quality but retain the flexibility to act opportunistically.

- We see opportunities in domestically focused industries that may benefit from deregulation while plan to limit exposure to sectors where revenues/costs could be negatively impacted by policy uncertainty